Are changes in the fair value of investment property an element of operating results?

Here’s another of the issues arising from extracts of enforcement decisions issued in the past by the European Securities and Markets Authority (ESMA) (for more background see here); this is from their 11th edition:

- “The issuer, a real estate company, presents changes in the fair value of investment property (separated in two lines for realized and unrealized)…in its profit and loss account after subtotals for operating results….

- The enforcer found that, whilst IAS 1 does not prescribe the presentation of fair value changes in the profit and loss account, the issuer should revise its presentation such that fair value changes be taken into account in the determination of operating results (IAS 1, Basis of Conclusions)….

- The enforcer was concerned that the presentation of fair value changes for investment property outside operating results is not in accordance with IFRS.

- The issuer noted that there are no detailed requirements in IAS 1 on how to present fair value changes in the income statement. The issuer indicated that many real estate companies use a similar presentation.

- The enforcer referred to IAS 1, Basis of Conclusions, paragraph 56, in which the following rationale is provided: “The Board recognizes that an entity may elect to disclose the results of operating activities, or a similar line item, even though this term is not defined. In such cases the Board notes that the entity should ensure that the amount disclosed is representative of activities that would normally be regarded as “operating”. In the Board’s view it would be misleading and would impair the comparability of financial statements if items of an operating nature were excluded from the results of operating activities, even if that had been industry practice. For example it would be inappropriate to exclude items clearly related to operations (such as inventory write-downs and restructuring and relocation expenses) be-cause they occur irregularly or infrequently or are unusual in amounts. Similarly, it would be inappropriate to exclude items on the grounds that they do not involve cash flows such as depreciation and amortization expenses.”

- The enforcer was of the view that fair value changes in investment property are a normal part of the activities of a real estate company that has opted to account for investment property in accordance with the fair value model under IAS 40 and which features in the issuer’s description of its business model.”

As with many of these summaries, it would be good to have a bit more detail on how “the enforcer” (as ESMA likes to term it) actually reached this conclusion (and on whether the issuer then merely caved on the matter, particularly given its observation about supporting practice). I imagine this might be one area where most practitioners, if adequately motivated, could build a multi-faceted argument in either direction. In the issuer’s favour, one might argue that the fair value changes can’t represent activities that would normally be regarded as “operating” if there’s enough evidence that many issuers in fact don’t regard them as such. One might argue that the examples cited above from IAS 1.56 only speak to the tracking of costs that are clearly being incurred or consumed by operations, and thus don’t say anything about how to look at the application of a fair value measurement model, which doesn’t involve such costs at all. One might argue that something arising purely from an accounting policy determination has nothing to do with “activities” as IAS 1 is using the term above. And so on…

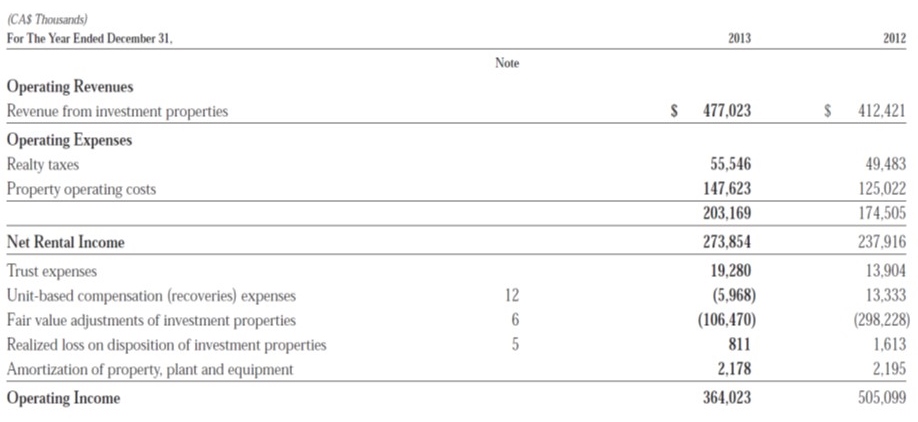

Certainly, this regulatory example hasn’t left much of a trace in the sands of time. I looked quickly at some Canadian real estate entities: many of them don’t disclose an “operating income”-type subtotal, but of the first three I found that do, one of them includes the change in fair value of its investment properties within that measure (Canadian Apartment Properties Real Estate Investment Trust)…

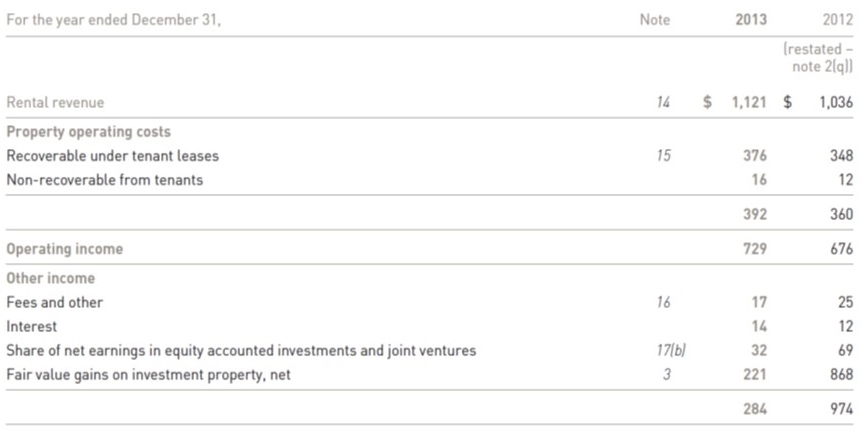

…and the other two don’t (Cominar Real Estate Investment Trust; RioCan Real Estate Investment Trust).

If you were so inclined, you could see this as a prime example of impaired comparability between financial statements. And Canadian regulators have certainly intervened in this broad territory in the past – it was covered, among other things, by one of the OSC’s longest-standing old staff accounting communiques (which related to old Canadian GAAP and was rescinded when IFRS came in), on income statement presentation. This said: “in staff’s view the exclusion of items that are directly related to Normal Business Activities from an income statement subtotal that is clearly intended to be representative of such activities is misleading and limits the comparability of financial information. This is particularly true when issuers in the same industry adopt different interpretations of operating income. To ensure comparability and to aress the existing practice problem, those issuers that choose to highlight an income statement subtotal such as operating income should include all items in that subtotal that are reasonably considered to be representative of Normal Business Activities.” The examples provided were similar to those currently contained in IAS 1, and of course didn’t include the fair value changes discussed above (which didn’t exist prior to implementing IFRS).

Some might say it’d be good to have greater consistency on this matter within the real estate industry. But what form would that consistency take? Beats me…

The opinions expressed are solely those of the author