Are certain kinds of disclosures actively prohibited under IFRS?

Here’s a disclosure to think about:

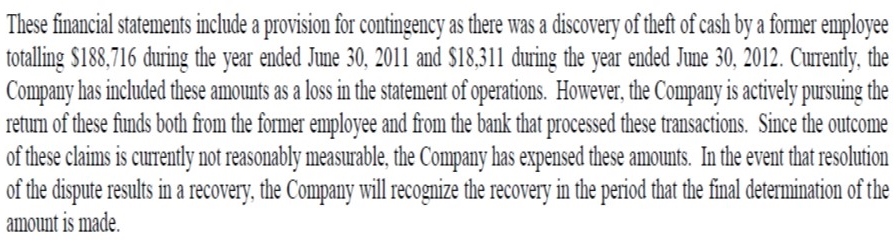

The amount that the company hopes to recover is, I think, a contingent asset – a “possible asset that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.” I assume that’s the case because it doesn’t seem to be entirely within the company’s control whether or not it’s successful in recovering any or all of the stolen amount. But then the question arises: is this disclosure – even of the broad fact that the company might recognize a recovery in a future period – actually in accordance with IFRS? IAS 37.89 says: “Where an inflow of economic benefits is probable, an entity shall disclose a brief description of the nature of the contingent assets at the end of the reporting period, and, where practicable, an estimate of their financial effect…” The standard doesn’t explicitly prohibit disclosing contingent assets not reaching that threshold, but at least one of the big firms takes the view in its literature that this is what’s intended, presumably on the basis that any possible benefit to investors of knowing about the situation would be outweighed by the risk of them placing too much weight on it (old Canadian GAAP was more specific on this point, saying “it would not be appropriate to disclose the existence of a contingent gain that is unlikely to be realized”).

If we assume for the sake of argument that’s what IAS 37 intends, then in this case (which of course I’m just using as a springboard to muse about the requirement in general – I don’t know anything about these specific facts), it doesn’t seem the existence of the contingent asset is necessarily probable. The company doesn’t say that it is, and based on the little information provided, it doesn’t sound like the outcome of the process can easily be anticipated. It seems to follow then that this disclosure might not be consistent with IAS 37.

I think most people would say this feels a bit different, because the company is just trying to get back what it originally owned. But the disclosure requirements for contingent assets don’t change based on how the issue arose – they’re based on where things stand now. And whether an entity is trying to remedy a black-and-white theft or launching a Quixotic legal action to seize something it never had in the first place, it comes down to the same thing – is the likelihood of obtaining that asset sufficient to justify talking about it? If not, then you might think IFRS requires remaining quiet.

(It’s possible on transition from old Canadian GAAP to IFRS a few years ago that companies might have found themselves needing to remove something they’d previously disclosed in this area. CICA 3290 said the existence of a contingent gain should be disclosed “when it is likely that a future event will confirm that an asset had been acquired or a liability reduced at the date of the financial statements.” The IFRS threshold of “probable” might be interpreted as being a bit more restrictive than the old threshold of “likely,” in which case items falling in the gap wouldn’t meet the criterion any more. But of course, even if an ongoing situation which used to be disclosed was subsequently eliminated from the statements because of this distinction, the information would remain out there, just as a jury can’t un-hear something it’s already heard, regardless that the judge struck it from the testimony.)

You might say the contingency wouldn’t be adequately described without highlighting these recovery attempts. But there’s another issue, that the expense side of this doesn’t seem appropriately labeled as a “provision for contingency” in the first place. The lost money doesn’t represent a possible obligation, or a present obligation that can’t be recognized for the reasons set out in IAS 37 – it’s just a loss, that nothing could justify not recognizing. It doesn’t even seem like a provision, a liability of uncertain timing or amount, because there’s no liability (so IAS 37.85, which says that for each class of provision, disclosure should include “the amount of any expected reimbursement,” isn’t relevant either).

By now you’re probably thinking this whole article is a ridiculous example of taking a sledgehammer to a nut. And indeed it is – no investor would rush to buy the company’s stock based on the vague prospect of this particular recovery action turning out well. But for the sake of argument, what if the amount being disclosed were much greater, one that could potentially transform the company’s prospects – should it then be restricted? You might say the world in general is full of such “disclosures” – what are those egregious lottery ticket commercials (“Imagine the freedom!”) if not an invitation to muse on the wonderful prospects of monstrously remote contingent assets? And, no question, some people are swayed by such advertising into spending money they shouldn’t. Is that an example of calculated wrongdoing by those making the disclosure, or just yet another example of the messy imperfections of human structures?

Whatever the answer, there’s something else to consider – it’s contrary to securities law to issue misleading disclosure, regardless of the requirements of IFRS. Disclosing some remotely attainable asset, if it’s sufficiently clear what’s going on, may not ultimately be of much utility to anyone, but it’s not necessarily misleading, no more so than whatever the company has to say about its far-off hopes and dreams in other aspects of its existence. On the other hand, perhaps some disclosures – even if they’re essentially telling the truth – are so potentially damagingly tempting to investors that the only reasonable thing to do is stamp them out. Perhaps…?

The opinions expressed are solely those of the author