These blog entries don’t usually lift such a big block of text from somewhere else, but in the circumstances it seems like the best way to go…

This is from the December 31, 2017 annual financial statements of Bombardier Inc.

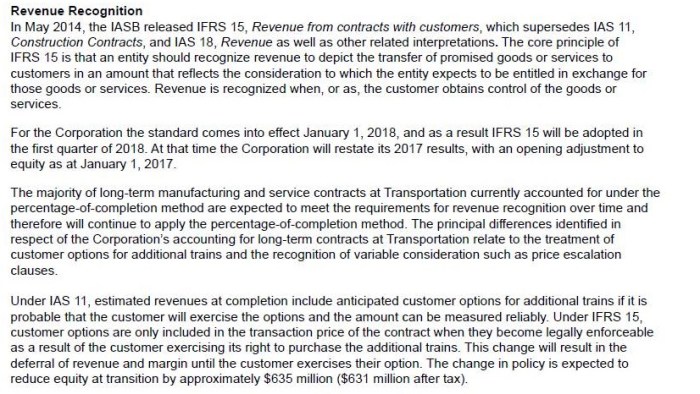

It might be concluded from all this that if Bombardier didn’t exist, students of IFRS 15 would have had to invent it. There may be a lot of them – the statistics for this blog indicate that people are searching on that issue more than on any other (accounting for girlfriends also makes the top five – conclude from that what you will). Let’s briefly unpack some of the main elements:

Customer options – “customer options are only included in the transaction price of the contract when they become legally enforceable as a result of the customer exercising its right to purchase the additional trains.” We looked at issues related to that here.

Variable consideration – “the concept of a constraint on the recognition of variable consideration whereby amounts can only be included in the transaction price to the extent it is highly probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.” We looked at that here.

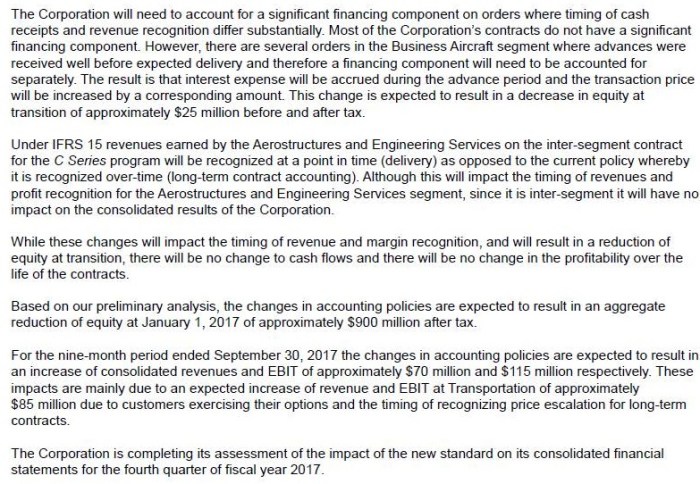

Financing component – “there are several orders in the Business Aircraft segment where advances were received well before expected delivery and therefore a financing component will need to be accounted for separately.” Although this concept existed in IAS 18, it’s much better defined in IFRS 15. We looked at that here as well.

We haven’t previously discussed the point relating to onerous contracts though. IAS 37.68 defines this as a contract for which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it. For onerous contracts falling under IFRS 15, this could be interpreted either as referring to costs an entity can’t avoid because it has the contract, or the costs it wouldn’t incur if didn’t have the contract. Under the first reading, for instance, the calculation of the costs might include a depreciation charge on any relevant assets, because using them to fulfill the contract makes that cost unavoidable. Under the second reading, you wouldn’t include such a depreciation charge on assets that are held and used for other purposes, because a depreciation charge would eventually be incurred on those assets regardless.

The IFRIC didn’t conclude on the correct reading, but noted an entity should apply its interpretation consistently to all onerous contracts. It’s continuing to study the concept of “unavoidable costs,” so there may be more on this in the future.

Will all of these changes make Bombardier’s financial statements in some meaningful sense “better”? I don’t know enough about the company to offer an opinion. For a lot of readers, their interest will presumably largely begin and end with the clarification that: “there will be no change to cash flows and there will be no change in the profitability over the life of the contracts.” Whereas the economics of a hypothetical company with only a single material contract might become clearer under IFRS 15, such clarity is likely to be blurred when multiple overlapping contracts exist. Some may interpret the fact that revenue will often be recognized later under the new model than it was before as a sign of greater “conservatism” (regardless that we know this isn’t the object of the standard, nor of any aspect of IFRS) and draw some broad additional comfort from that; likewise from the basic fact of knowing that the work of implementing the standard has caused the company’s revenue recognition models to be examined in detail. As we know, it’s awfully difficult to draw even generalized cause-and-effect relationships between a company’s accounting policies and the investment decisions that get made about it. But it’s perpetually tempting to try…

The opinions expressed are solely those of the author.