Let’s take a look at some other recent examples of changes resulting from the implementation of IFRS 15.

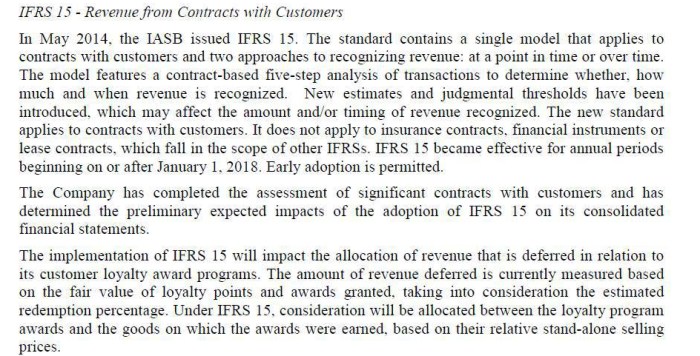

This is from Reitmans (Canada) Limited:

As we’ve discussed before, for purposes of the first issue, the stand-alone selling price is the price at which an entity would sell a promised good or service separately to a customer. IFRS 15 states: “The best evidence of a stand-alone selling price is the observable price of a good or service when the entity sells that good or service separately in similar circumstances and to similar customers. A contractually stated price or a list price for a good or service may be (but shall not be presumed to be) the stand-alone selling price of that good or service.” If a stand-alone selling price isn’t directly observable, the entity estimates it in the way that achieves the standard’s allocation objective, considering all information (including market conditions, entity-specific factors and information about the customer or class of customer) reasonably available to it. IFRS 15 requires maximizing the use of observable inputs and applying estimation methods consistently in similar circumstances.

The standard allows an entity to estimate the observable stand-alone selling price for a particular performance obligation on a residual basis (that is, based on what’s left of the transaction price after computing the amounts to be assigned to other goods and services), but only when the selling price is highly variable because a representative stand-alone selling price isn’t discernible from past transactions (that is, the evidence shows the item is sold in practice for a broad range of amounts), or when the entity hasn’t yet established a price for that good or service and the good or service hasn’t previously been sold on a stand-alone basis (i.e. the selling price is inherently uncertain). Otherwise, a residual basis isn’t acceptable under the standard.

The basis for conclusions emphasizes a key point, that applying the residual method under IFRS 15 “cannot realistically result in a stand-alone selling price of zero if the good or service is in fact distinct because to be distinct that good or service must have value on a stand-alone basis.” This shuts down what might otherwise have frequently been an appealing way of rationalizing down the detailed number-crunching. It emphasizes further that if the residual approach results in “no, or very little consideration being allocated to a good or service or a bundle of goods or services, the entity should consider whether that estimate is appropriate in those circumstances.” Of course, materiality considerations still apply here as they do to everything, but the emphasis here seems to provide a brake on merely asserting immateriality too sweepingly (parallel questions sometimes arise in other areas of IFRS about whether that’s the case, for instance relating to assertions that the equity component of a convertible financial instrument hasn’t been separately recognized on the basis of immateriality).

I don’t think we’ve covered the “breakage” issue before. We’ve covered the fact that the contract is presented in the balance sheet either as a contract asset or a contract liability, depending on the relationship between the entity’s performance and the customer’s payment. A contract liability represents an obligation to transfer goods or services to a customer for which the entity has received consideration, but sometimes customers don’t end up exercising all those contractual rights – this is what’s known as “breakage.” As Reitmans indicates, if an entity expects to be entitled to such a breakage amount, it recognizes the expected amount as revenue in proportion to the pattern of rights exercised by the customer. The basis for conclusions observes that this “effectively increases the transaction price allocated to the individual goods or services transferred to the customer to include the revenue from the entity’s estimate of unexercised rights” and that this makes sense because in concept, if the entity didn’t expect any breakage, it might increase the price of its goods or services: “For example, an airline that sells non-refundable tickets would presumably charge a higher price per ticket if there was no expectation of breakage.” However, this only applies if it’s highly probable that recognizing revenue for breakage won’t result in a subsequent significant revenue reversal (similar to the constraint applying to the inclusion of variable consideration in the transaction price).

As for the matters relating to rights of return, we looked at those here.

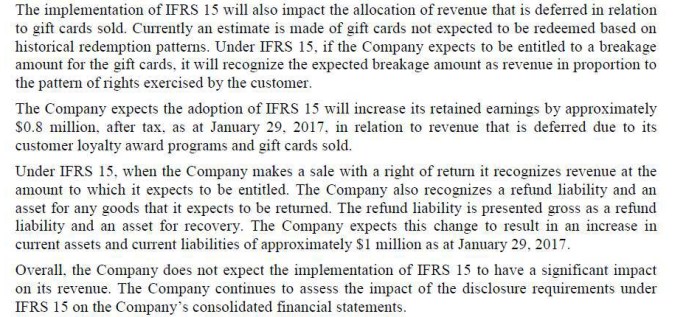

It’s perhaps interesting to note that Reitmans’ description of its existing accounting policy for revenue consumes only 137 words, most of them devoted to gift cards and loyalty programs. The description of the core revenue recognition policy is only 32 words:

- Revenue is recognized from the sale of merchandise when a customer purchases and takes delivery of the merchandise. Reported sales are net of returns and estimated possible returns and exclude sales taxes.

So the disclosure of the future impact of IFRS 15 is more than three times as long as what the company has habitually said on this area in the past, and that’s just to conclude that the new standard won’t have a significant impact on its revenue. It’ll be interesting, for this and for many other companies, to see what this portends about the volume and quality of ongoing disclosures…

The opinions expressed are solely those of the author