How can investors identify purpose-led companies? asks a recent publication from A Blueprint for Better Business.

This is an independent charity which says of itself: “We are not a consultancy or funded by business. We are a catalyst to help businesses be guided and inspired by a purpose that benefits society. Our work is about stimulating and energizing a different way of thinking and behaving in business.”

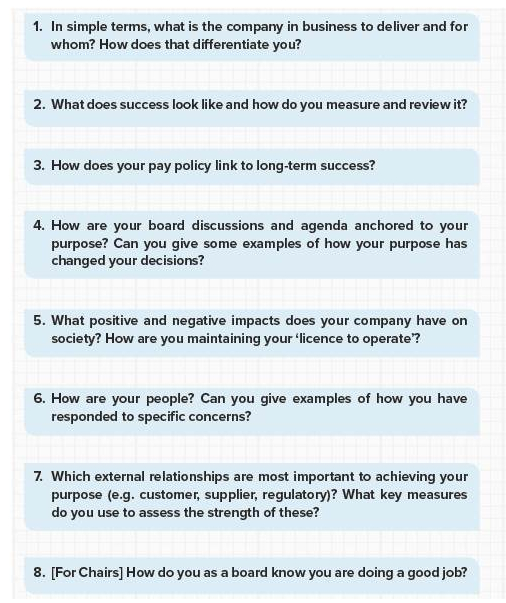

The publication notes a “renewed focus on purpose” in the corporate world and in society more generally, posing the question: “how can an investor tell the difference between a company which has undergone a slick communications exercise and one which is genuinely pursuing a purpose beyond profit, through which it seeks to generate its returns to investors?” To this end, it sets out the following questions “designed to stimulate deeper conversation, encouraging personal rather than pre-scripted answers, and to explore the depth of thinking and consistency with operational priorities”:

The publication is under no illusions that these questions, in themselves, will always provide clarity; a seasoned bunch of spin masters could obviously craft wondrous self-serving lies in response to all of them. The most obvious example is perhaps “How does your pay policy link to long-term success?” – any major entity’s executive compensation consultants will no doubt have pages of ready-made responses to such a question, professing “benchmarking” and “alignment with stakeholders” and “accountability” and all the rest, none of it standing in the way of inexorable bonus increases, regardless of broader fortunes. In many cases, it might be better to concede that the pay policy won’t in any major way link to long-term success, and to work around the issue to search for offsetting guarantees of virtue. I guess the writers of the publication would urge greater optimism on my part…

Anyway, the underlying question, of how one distinguishes the good answers from the bad ones, links to our earlier musings on character in financial reporting. Looking back at what I wrote then, I liked some of it enough to reproduce it here:

- …such readings (of an organization’s culture or character) are heavily conditional on context, and may be susceptible to misinterpretation. Similar observations might apply to any other apparent revelation of character by an entity’s financial reporting. For one thing, an amoral character may conceal his nature under an apparently seamlessly virtuous surface (as the old saying goes: sincerity is everything – once you can fake that, you’ve got it made). Beyond that, the determination of “character” on an entity-wide level entails an almost impossible tangle of complexities, with no objective basis of resolution. To take just one example that reflects the current political divide in the US in particular, some might detect character in an oil company’s efforts to “green” its activities, to report openly on its impact on the environment, and so forth. Others might see such efforts as weakly hypocritical or outright pointless, and find character only in the proud assertion of independence and profit maximization. The Economist recently opined that “this week showed that (Donald Trump) does not have the character to change,” but others take the measure of his character exactly in the refusal to do so.

- Still, it would surely be useful if every reporting entity (perhaps at the audit committee or disclosure committee level) were periodically to ask itself how it understands its own character, whether the tone and content of its corporate reporting fairly reflect this understanding, and what needs to be changed to clarify this (rather than, one hopes, to hide it). Such a project may focus on the MD&A and other communications more on the financial statements, but…it shouldn’t be solely that. David Thomson wrote years ago that the films of director Howard Hawks reflect the principle “that men are more expressive rolling a cigarette than saving the world.” To observe that such expression of character may also be found in the nuances of drafting an accounting policy hardly carries the same ring, but perhaps we can hope for it to hold true once in a while…

Picking up on that, a practical problem with the Blueprint for Better Business questions is that only the most privileged investors will have the ability to ask them directly of an entity’s key people, to study the delivery of the answer up-close, and then (as every worthwhile interlocution demands) to ask follow-up questions, to drill down on areas of avoidance and ambiguity and so on. That’s why boards and senior management should take it upon themselves to consider the questions, to imagine they’re being grilled on them by the world’s most astute (although fair-minded) interviewers, to identify the responses they’d hope to provide to that interviewer to be able to walk away with their heads held high, and then to put out that information whether it’s been asked for or not, in whatever form (or mixture of forms) makes most sense. After all, a company inspired by a true sense of purpose, beneficial to society, should be more than eager to talk about it, and thereby, presumably, to contribute to actually achieving it…

The opinions expressed are solely those of the author