At its July 2018 meeting, the Accounting Standards Advisory Forum discussed among many other things, the IASB’s plan to carry out a targeted standards-level review of disclosures.

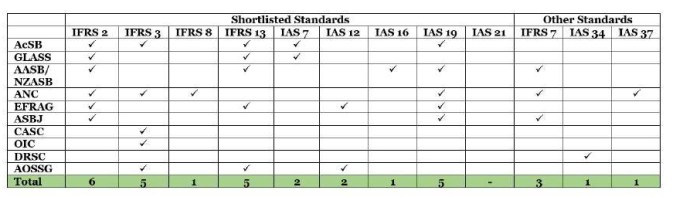

The discussion covered both the Board’s process for developing and drafting disclosure objectives and requirements, and which standards the Board should select for review. On the latter point, the meeting participants were given a shortlist of possibilities; some of them threw in other suggestions as well. Here’s a summary of the standards that had some support (to identify the participants, refer to the meeting notes – as you can see, some of the participants voted for five or six possibilities, others just for a single one.

You’ll note that the 10 participants cast votes for 11 different standards. By my quick count there are only some 39 standards to choose from (if we take everything subsequent to IFRS 13 as being too new for this purpose) and some of them either don’t have disclosure requirements (IFRS 10, IFRS 11) or would likely be too minor or esoteric or fact-specific to be the focus of this exercise (IFRS 1, IAS 20, IAS 27, IAS 29). Depending on how you make those judgments, as many as half of the plausible candidates for review may have received a vote from one or more of the participants. Also interesting are the reasons cited by the participants for making their selections:

- IFRS 3 does not require information that users would find useful in their analysis, and there is diversity in practice regarding disclosures provided about business combinations.

- IFRS 13 Fair Value Measurement … contains all disclosure issues identified during the Principles of Disclosure project, including a lack of clear disclosure objectives.

- IAS 19 or IFRS 2 – entities do not understand the disclosure objectives in either of these standards and provide excessive information in their financial statements about employee benefits and share-based payments. Furthermore, the information disclosed in financial statements about share-based payments is often boilerplate and does not provide all the information that users need in assessing corporate governance.

- IAS 12’s disclosure requirements are focused on the accounting technicalities and do not require information that users would find useful in their analysis

- IFRS 8 Operating Segments should be selected because it does not require all the information that users would find useful in their analysis.

- IFRS 7 includes unclear disclosure objectives and disclosure requirements that do not provide relevant information about some non-financial entities.

- IAS 37 Provisions, Contingent Liabilities and Contingent Assets should be selected because… it does not require all of the information that users would find useful in their analysis.

- IAS 34 Interim Financial Reporting should be selected because…the Board should consider how the Guidance for the Board can be applied to forms of financial reporting other than the annual report.

Of course, this is just a summary. But it’s still notable that only IAS 19 and IFRS 2 are being cited explicitly for excessive disclosure requirements; most of the others are being cited for not requiring at least some information that users would find useful. Clearly, as written, that means participants were thinking of additional disclosures that should be added. Perhaps in some cases they could point to existing disclosure requirements that could be removed to even things out, although for some of the cited standards (like IAS 37) it’s hard to see how that would be possible.

The first part of the discussion contained some astute observations relevant to this:

- the EFRAG and AASB/NZASB members said that users should be asked why they need the requested information and how they expect to use it. They added that this would provide deeper insights for developing robust disclosure objectives. The AASB/NZASB member said that it would also be useful to understand how often users expect to use the requested information. The FASB member noted that in their similar initiative, they focused on asking users why the requested information is useful. However, the FASB member advised against specifying in the Standard how the information will be used because investors use information in different ways.

No doubt those members wouldn’t ever put it this way, but the subtext is that it’s easy for users, if they’re asked, to complain about the absence of this and the inadequacy of that, and to throw out a wishlist of enhanced disclosures. But likewise, in other walks of life, most of us will probably say yes, if asked whether we’d be in favour of having more choice in one respect or another. We might even believe as we speak that we’d exploit these choices if they were available. But in practice, it often doesn’t work out that way, given limitations of time, resources and behavioural capacity (see for example the paradox of choice). In truth, one of the worst ways of figuring out how to address a complex challenge is to ask a whole bunch of people for their opinions about it.

And then it’s hard to think this through without coming back, as we perpetually do, to technological issues. This is just briefly mentioned in the meeting notes: “(a member) said that the Board should consider the effect of digital reporting, for example, whether advances in digital reporting will affect the extent to which disclosures are separated from the primary financial statements.” Indeed, if the premise behind future additions to disclosure requirements is that users will often be carrying out an “analysis” in which those items are relevant, then it can’t possibly be a great hardship to ask those users to click on a few links to access some of those disclosures. Put another way, an analysis which couldn’t spare the time, or couldn’t access the technological capacity, to do that much, would be unlikely to be very sound or reliable overall. No matter what some users might say…

Anyway, the last thing we knew, the Board’s tentative selections were IAS 19 and IFRS 13. We’ll see if that changes…

The opinions expressed are solely those of the author