Here’s the background to another issue recently discussed by CPA Canada’s IFRS Discussion Group:

- Paragraph 12 of IAS 41 Agriculture states that “[a] biological asset shall be measured on initial recognition and at the end of each reporting period at its fair value less costs to sell [FVLCS], except for the case described in paragraph 30 where the fair value cannot be measured reliably.”

- Once the cannabis plant has been harvested, the costs incurred thereafter are within the scope of IAS 2 Inventories. However, questions arise with regards to how to account for the costs incurred related to the biological transformation of the biological asset between the point of initial recognition and the point of harvest (also referred to as “subsequent expenditures”).

- Paragraph B62 of the Basis for Conclusions on IAS 41 states, in part, that “[t]he Board decided not to explicitly prescribe the accounting for subsequent expenditures related to biological assets in the Standard, because it believes to do so is unnecessary with a fair value measurement approach.”

By now, of course, the IASB is probably more fully aware of the necessity of explicitly prescribing everything, principles-based approach notwithstanding. Anyway, in the absence of such prescription, the possibilities for how to treat the such subsequent expenditures are as follows:

- They should be expensed, so that they don’t affect the amount reported as change in FVLCS;

- They should be capitalized to the carrying value of the biological asset, therefore reducing the amount that would otherwise be reported as change in FVLCS. Under this approach, the change in FVLCS would more purely reflect the natural growth of the plant and changes in relevant external factors;

- It’s a matter of choice.

Most of the group members concluded it’s a matter of choice, although some of them also thought that capitalizing the subsequent costs would contribute to a more meaningful gross profit figure. The group also discussed the kinds of subsequent expenditures that should be capitalized, where that’s the chosen policy – in particular whether that issue is best assessed by analogizing to IAS 2 Inventories or to IAS 16 Property, plant and equipment. Although the two would often get to the same place, it might not always go that way. For example, IAS 2 talks about the cost of administration as being a part of fixed production overhead, and requires that these be systematically allocated to the cost of conversion of inventories. In contrast, IAS 16 lists administration costs among the items that are not costs of an item of property, plan and equipment. There was a diversity of views on this.

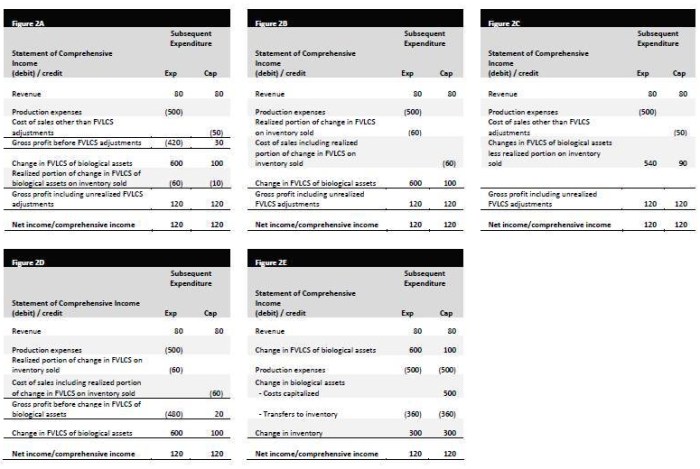

The group then discussed how all of this might best be presented in the income statement. You can refer to the report for the underlying detail, but the five illustrations below largely speak for themselves. In each case, the left hand column assumes subsequent expenditures are being expensed; the right hand column assumes they’re being capitalized.

We’ve looked in the past at the widespread unhappiness with IAS 41 insofar as it applies to marijuana, and at the view that it obscures performance rather than illuminating it. It seems that a consistent form of income statement presentation from one entity to the next might alleviate this to some extent, if only by allowing a consistent basis for developing adjusted non-GAAP measures. However, not surprisingly, there was no unified view on this either (the group referred all of these matters to the Accounting Standards Board, for possible referral to the IASB or to IFRIC). The points made by the group include:

- IAS 1 and IAS 41 don’t prescribe any specific presentation for changes in the FVLCS of biological assets. Entities must consider the users of their financial statements and provide information that is sufficiently disaggregated and transparent to determine what is or isn’t included in the line items presented.

- Whether an entity expenses or capitalizes subsequent expenditures may be relevant in determining the most appropriate presentation of gross profit subtotals. You might take the view that for an entity that expenses those expenditures as incurred, a gross profit subtotal including expenditures related to items not yet sold would be less appropriate (and presumably less consistent from one period to the next).

- If you regard gross profit as being solely a measure of realized margin over cost of goods sold, as many do, then it might seem to follow that it’s not appropriate to present a gross profit measure that includes unrealized changes in FVLCS of biological assets.

As we know, the format of the income statement, and the desirability or necessity of defining various subtotals, are under active discussion by the IASB; we also know that these issues by their nature belong more to an old paper-based world than to one of artificially-enhanced investing. But as this sector, for now at least, is likely disproportionately interesting to retail investors, some clarity would certainly be welcome. Whether it can come in time to save some of them a certain amount of self-inflicted pain may be in question…

The opinions expressed are solely those of the author