Some of the issues arising in deferring gains, rather than recognizing them immediately

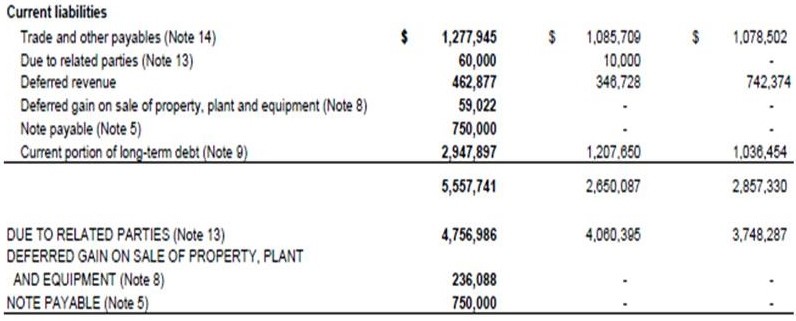

Here’s an extract from some financial statements of a few years ago:

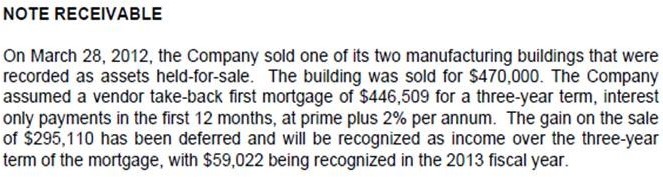

Here’s the note that discusses the deferred gain:

I should emphasize at the outset that I’m just using this interesting disclosure as a springboard to muse on the general issue, rather than to comment on this specific situation, which I know nothing about. But I don’t believe IFRS addresses this situation specifically. IAS 16 simply says that the gain or loss arising from derecognizing an item of property, plant and equipment is determined as the difference between the net disposal proceeds and the item’s carrying amount. Any financial instruments making up the net disposal proceeds are typically recognized initially at their fair values, and then the calculation of the gain or loss follows on from there: even if some of these financial instruments involve an ongoing contractual relationship with the acquirer, IAS 16 doesn’t suggest this might require deferring any gain. It does say that if payment for an item is deferred, then the consideration is recognized at the cash price equivalent, with the difference between this amount and the nominal amount recognized as interest revenue over the term of the receivable. But again, this doesn’t mean the gain on disposal would be deferred, only that the amount recognized would better reflect the economics of the transaction.

IAS 17 sets out a situation where a gain or loss might be deferred and amortized, relating to situations where a sale is followed by leasing back the same asset, and the sale price doesn’t clearly represent fair value. But this doesn’t seem to apply to the situation here, at least from what we can tell: it says the company assumed a mortgage as part of the consideration, but doesn’t suggest it’s continuing to use the property.

Old Canadian GAAP addressed something along these lines in EIC-79 Gain recognition in arm’s-length and related party transactions when the consideration received includes a claim on the assets sold. This described a situation where a seller receives a note or other financial instrument issued by the purchaser, and where in collecting the amounts due under the note, the seller has recourse in effect only against the assets sold – for instance, because the purchaser doesn’t have any other significant assets. EIC-79 concluded that that the seller “should recognize the gain on the sale in its income only to the extent that the gain is realized… when: (a) there is a substantial commitment by the purchaser demonstrating its intent to honour its obligations under the note; and (b) the seller has reasonable assurance of collecting the note.” It stated: “The seller would recognize a gain in income when the conditions for realization described above are first satisfied, whether at the date of the sale or subsequently. If the criteria are not satisfied at the sale date, the seller would defer the gain.” This didn’t seem to envisage though that the gain would be deferred and amortized – once the appropriate conditions existed, the gain would be recognized in full. Anyway, that’s all history. The SEC had also addressed various related situations in its staff accounting bulletins, but as far as I can tell, these have now been removed.

Still, it’s not hard to see the appeal of the kind of approach this company applied. Although conservatism doesn’t have a place in the financial reporting framework, it’s often viewed (rightly or wrongly) as a virtue nevertheless, and accountants have a particular aversion to recognizing gains that might not seem justified by subsequent developments (even if they know these technically shouldn’t matter). If the face value of the vendor takeback mortgage doesn’t equal its fair value – whether because it has a below-market interest rate attached, or because of the credit risk attaching to the counterparty, or for other reasons – then this might have been addressed by recording the instrument at an estimate of that lower fair value, and then recognizing higher interest income over its life. But this would still have meant recognizing a gain at the outset, albeit a smaller one. One could avoid recognizing a gain by recording the fair value of the consideration received as being equal to the carrying value of the property disposed of, but that’s entirely arbitrary, and would obscure the fact that the company presumably believes it did make a gain on the transaction and will ultimately realize that gain. Crunch all of those considerations and you might conclude it’s most reasonable to recognize the gain over time, in line with the performance of the mortgage.

As I said, that may not at all reflect the thought process applying in this particular circumstance. But anyway, it prompts a useful cautionary note: if care has to be taken in recognizing a calculated gain, then simply deferring and amortizing that same amount of gain isn’t necessarily an uncontroversial back-up solution. It might by some measure provide a more “conservative” picture of the transaction, but that doesn’t mean it’ll always be a more appropriate one.

The opinions expressed are solely those of the author