When Canada was first learning about IFRS, the IAS 16 revaluation model probably received disproportionate attention, largely just because it was easy to talk about (to a point anyway). As it turned out, very few Canadian companies actually chose this option – almost all of them stuck with the familiar cost model. A couple did take the plunge though. Here’s an example from Urban Communications Inc:

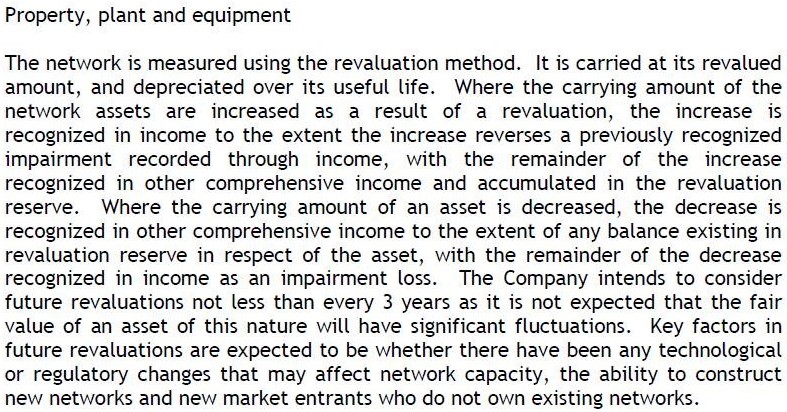

Urban is “a telecommunications company that develops and operates telecommunications networks in urban areas and provides a full suite of Internet, voice, video and broadband application products over its state-of-the-art carrier grade fibre optic network.” Presumably the company perceived its investment in the network as being central to the value proposition it represents, thus driving its choice of the policy. To illustrate – at the end of December 2013, the network had a carrying value of $4.8 million (total assets were just $5.2 million); of this, the balance in the revaluation reserve was $3.0 million. Urban didn’t apply this policy to its other classes of property and equipment, all of which are far less significant. Anyway, in 2014 Urban switched to using the cost model, making examples of the revaluation model even harder to find in practice (as an aside, some might question – at least in some circumstances – whether a change from a fair value to a cost model results in financial statements providing “more relevant” information, as required for a change in accounting policy, but never mind).

This is an aspect of IFRS where the original “basis for conclusions” document suggests the IASB might have revisited things by now: “The Board is taking part in research activities with national standard-setters on revaluations of property, plant and equipment. This research is intended to promote international convergence of standards. One of the most important issues is identifying the preferred measurement attribute for revaluations. This research could lead to proposals to amend IAS 16.” I’m not sure what came of that research, but the website doesn’t seem to contain any hint about revisiting the standard in the foreseeable future.

And really, why would it? If the choice of the revaluation model didn’t already exist in IFRS, it’s unlikely too many people would lobby for it in its current half-hearted form: it has the feeling of a conceptual flourish they indulged themselves with in less politically-charged times. Although by its nature it creates an inconsistency between companies, it’s not one that’s likely to affect key performance indicators as people currently perceive them (it wouldn’t affect cash flow, most obviously). And if the details of the model are inherently arbitrary, well, it doesn’t matter – I doubt anyone looks at the revalued amounts as being a particularly rigorous measure of anything. The very act of choosing the revaluation model for a class of assets sends a message about the perceived limitations of assessing those assets solely by referring to their cost – beyond that, I doubt investors would put too much weight on the specific value assigned to them.

IAS 16 seems to anticipate this when it says that while some items might require annual revaluations, “such frequent revaluations are unnecessary for items of property, plant and equipment with only insignificant changes in fair value. Instead, it may be necessary to revalue the item only every three or five years.” Urban’s intended policy of considering future revaluations not less than every three years was entirely consistent with this. But if the revaluation model was really intended to provide a quasi-meaningful snapshot of fair value, it would be rather remarkable to allow such an easygoing approach to the issue….

IFRS 13 Fair value measurement applies to fair value determinations made for the purpose of the IAS 16 revaluation model, and although it doesn’t specifically contradict the “only every three or five years” stipulation, it seems by its nature to put some strain on it (and to introduce some new complexities, such as the “highest and best use” valuation premise it applies to non-financial assets). In determining that it’s only necessary to revalue the item on that schedule, the entity now has to establish throughout the intervening period that the carrying amount doesn’t differ materially from the amount that would be “received to sell (the asset)…in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions.” This focuses more specifically than before on what market participants would actually do, and for many assets it might be a bit difficult to say that what they’d do wouldn’t change over the course of several years (particularly where the assets are subject to competitive pressures, technological change and so forth).

For the rest of it, well, I guess we’ve all at some point had to sit through some instruction on the mechanics of recognizing a revaluation deficit when it reverses a previous surplus, or vice versa, and I guess we’re all glad we never had to spend more time on it than that. Indeed, the time I spent to rescue this brief article from the archives and give it a slight updating constitutes my entire engagement with the issue over the last few years. Which feels about right.

The opinions expressed are solely those of the author.