Let’s look at another recent disclosure about the impact of IFRS 15.

Here’s an extract from what SNC-Lavalin Group Inc. had to say:

Let’s pick out a few of the items there:

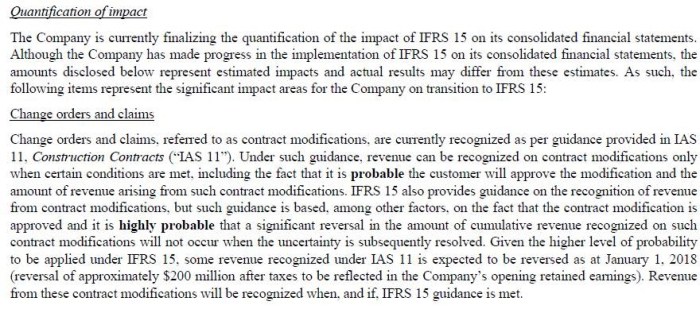

Variable consideration We’ve noted before that an entity doesn’t include any amount of variable consideration in the transaction price unless “it is highly probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.” This might apply for instance when the entity only has limited experience with a particular product, or where the range of concessions that might be offered to customers is unusually wide or unpredictable. The entity updates its assessment of these matters at the end of each reporting period, along with updating other aspects of its assessment of variable consideration.

The same constraints apply in recognizing variable consideration arising from modified contract terms. The company sets out a distinction between estimates it might assess as “probable” of not reversing, and those it can assess as “highly probable.” There’s an illustration here though of the slipperiness of such terms and of how they depend on context. The standard’s basis for conclusions underlines that IFRS is using “highly probable” to indicate the same level of confidence that US GAAP denotes by the term “probable” (defined in US GAAP as “the future event or events are likely to occur” but in IFRS only as “more likely than not”): it says “to achieve the same meaning in IFRS as US GAAP, the boards decided to use the term ‘highly probable’ for IFRS purposes and ‘probable’ for US GAAP purposes.” IFRS 5 had previously specified that “highly probable” is “significantly more likely than probable,” or put another way – significantly more likely than (merely) more likely than not. I’m not sure whether we can take these distinctions to reflect general non-accounting usage though – for example, when the New York Times recently reported one individual as arguing that “the Trump administration’s new nuclear strategy involved the manufacture of low-yield weapons and made nuclear war more probable,” we can only hope it wasn’t to be read from an international perspective as “more highly probable”…

Accounting for warranties We wrote about that issue here, noting the following:

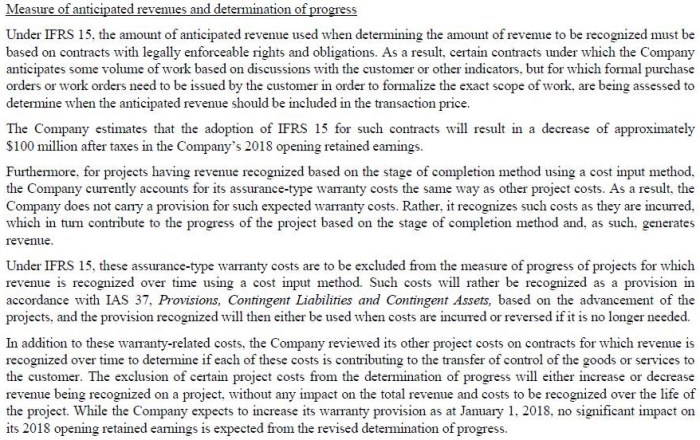

- some warranties only provide a customer with assurance that the related product will function as the parties intended because it complies with agreed-upon specifications; other warranties provide the customer with other services as well. If the warranty only provides assurance that the product complies with agreed-upon specifications, then it doesn’t constitute a separate performance obligation (rather, as you might put it, it supports the performance obligations that have already been entered into). In this situation, the warranty falls under IAS 37 Provisions, Contingent Liabilities and Contingent Assets. The first of the illustrative examples attached to IAS 37 addresses a typical kind of warranty arrangement, concluding that the manufacturer (in that particular example) recognizes a provision for the best estimate of the costs of making good under the warranty products sold before the end of the reporting period. It follows under the IAS 37 model that an entity doesn’t make a provision if it’s not probable that an outflow of resources will be required to settle the obligation, or if a reliable estimate can’t be made of its amount (although that latter situation should be rare).

SNC’s new policy seems to flow exactly from this guidance on warranties that don’t constitute a separate performance obligation.

Project costs The reference to “(reviewing) its other project costs on contracts for which revenue is recognized over time to determine if each of these costs is contributing to the transfer of control of the goods or services to the customer” seems to reflect the greater precision under IFRS 15 regarding what might fall within such costs and conversely, the standard’s explicit listing of certain kinds of costs to be recognized as expenses when incurred. Although the standard is called “Revenue from Contracts with Customers,” we may – who knows – identify some cases over time where the bottom-line impact flows as much from the impact on reported costs as from that on top-line revenue…

The opinions expressed are solely those of the author