The IASB has issued Guide to Selecting and Applying Accounting Policies – IAS 8.

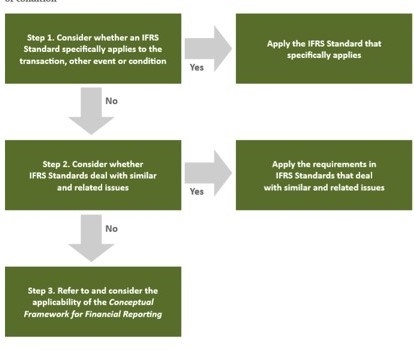

The stated objective, just as the title suggests, is to explain how to apply the IAS 8 requirements for selecting and applying accounting policies for transactions, other events and conditions, using material and examples that have been discussed by the IASB and IFRIC. This is the summary of the landscape:

The publication’s purpose is a bit obscure to me anyway – at just 12 pages long (including front and back covers) it doesn’t break any new ground, seeming just to constitute a compilation of previously-issued material. Still, it’s perhaps most instructive to try reading it as if through a pair of unfamiliar eyes: to the extent I could assume such a role, it left me a bit perplexed.

For instance, it addresses a case where a “government charges a levy on entities as soon as they generate revenue in 2021. The amount each entity pays is calculated by reference to the revenue it generated in 2020. The levy is within the scope of IFRIC 21 Levies. An entity’s reporting period ends on 31 December 2020. The entity generates revenue in 2020, and in 2021 it starts to generate revenue on 3 January.” Applying IFRIC 21, the guide rapidly concludes that the entity first recognizes a liability on January 3, 2021, the date of the event that triggers the payment of the levy. But then it goes on:

- If the entity were to apply the concepts in the Conceptual Framework, it might recognize a liability earlier. Applying those concepts, the liability to pay the levy would be viewed as arising when the entity: (a) has already obtained economic benefits or taken an action and, as a consequence, will or may have to pay a levy that it would not otherwise have had to pay; and (b) has no practical ability to avoid paying the levy.

The publication asserts again that the entity applies the specifically applicable requirements of IFRIC 21, not the concepts of the conceptual framework. But – again, trying to look through unfamiliar eyes – this skips over an obvious question: why would such a mundane-sounding issue be subject to specific requirements that don’t align with the conceptual framework, especially when the resulting treatment may sound inferior. Those who spend some time in the IFRS universe may be familiar with the problem (as articulated on the current project page) but otherwise, the example is likely to raise as many questions as it answers.

Other aspects of the publication lay on the “if” and “might” and suchlike so heavily that you wonder if it’s saying anything even vaguely definitive. For example, it addresses the following scenario:

- A bank borrows gold from one party (contract 1) and then lends that gold to another party for the same term and for a higher fee (contract 2). The bank enters into the two contracts in contemplation of each other but the contracts are not linked. In each contract, the borrower obtains legal title to the gold at inception and has an obligation to return, at the end of the contract, gold of the same quality and quantity as that received. Each borrower pays a fee to its lender over the term of the contract but there are no cash flows at the inception of the contract.

The accompanying commentary includes the phrases “might conclude” (twice), “might be viewed,” “might judge,” once again ending on: “The policy developed might not be the same as one that the preparers would have developed if they had instead referred to the Conceptual Framework definitions.” If we assume that each such usage leaves at least some room for its antithesis (you might conclude, but then you might not; you might judge that way, but then you might judge another way…) then a reader might end up tangled deep in the branches of a rather dense decision tree (although on the one hand, he or she might not). A footnote takes the reader to a relevant IFRIC agenda decision, which provides a significant context absent from the IAS 8 publication – namely IFRIC’s conclusion that any narrow-scope standard-setting activity on that specific matter would be of limited benefit to entities and would have a high risk of unintended consequences.

Summing up, the publication would likely give the unschooled reader (and again, what other kind is it for?) the impression that the standards cover far less territory than they actually do. But at the same time, for those situations not covered by the standards, the guidance is vague, side-stepping some of the central questions altogether. For instance, it observes that “management may also consider the most recent pronouncements of other standard-setting bodies that use a similar conceptual framework to develop accounting standards, other accounting literature and accepted industry practices,” but has not a single word on how to apply those rather vague notions. But then, maybe that aspect of IAS 8 is almost meaningless anyway – after all, you can’t stop management from “considering” any nonsense it likes, as long as nothing ultimately rides on it…

The opinions expressed are solely those of the author